— Los Angeles, California By Astrid Gold

There’s a new American milestone, and no, it’s not buying your first home or paying off your student loans.

It’s this:

You can afford everything you need… and almost nothing you actually want.

According to a new The Washington Post poll, most Americans aren’t financially collapsing—but they’re also not moving forward. They’re stuck in a strange in-between space where survival is possible, but progress feels out of reach.

Welcome to the Treading Water Economy.

Barely Making It… Is the New Normal

The data is blunt.

- 53% of Americans say they have just enough to maintain their current lifestyle

- No extra savings

- No upgrades

- No breathing room

That means more than half the country is essentially one unexpected bill away from a problem.

You can pay your rent.

You can buy groceries.

You can keep the lights on.

But try to do anything beyond that—take a vacation, replace your car, go out to dinner regularly—and suddenly you’ve entered what now qualifies as “luxury spending.”

Yes, dinner out is now flirting with luxury status. Let that sink in.

The Middle Class Didn’t Disappear—It Got Repriced

For years, economists debated whether the middle class was shrinking.

They missed the real story.

The middle class didn’t vanish.

It got rebranded.

What used to be standard:

- Eating out once or twice a week

- A yearly vacation

- A reliable new car

Now feels like:

- Occasional indulgence

- Careful budgeting

- Or outright unaffordable

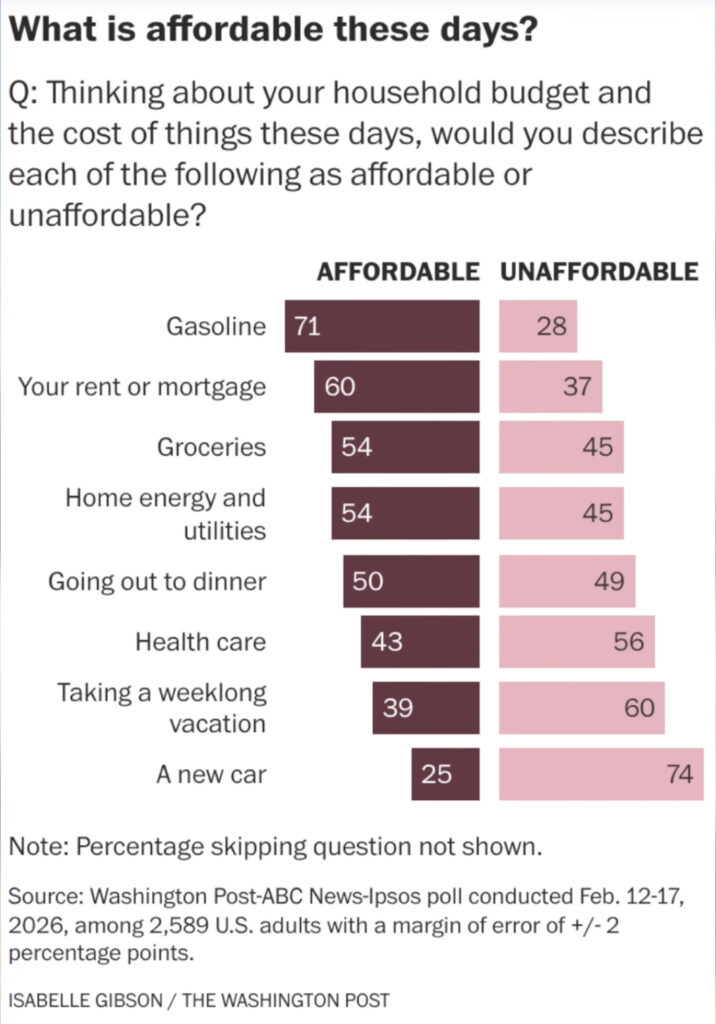

Half of Americans now say going out to eat is too expensive.

Healthcare? Forget it.

A week-long vacation? Aspirational.

A new car? Practically mythical.

And yet, incomes haven’t collapsed.

Which brings us to the real issue.

The Raise That Changes Nothing

Here’s the modern financial paradox:

You make more money… and feel exactly the same.

Or worse.

Because every time income rises, so does everything else:

- Rent adjusts upward

- Insurance creeps higher

- Groceries quietly climb

- Interest rates make borrowing more expensive

So the raise that should move you forward just keeps you in place.

That’s not a coincidence. That’s how the current economic structure behaves.

Even Six Figures Isn’t Safe Anymore

Once upon a time, $100,000 a year meant you’d made it.

Today—depending on where you live—it means you’re… stable.

Maybe.

In places like Los Angeles, where I’m writing this, six figures can evaporate quickly:

- $3,000+ rent

- Health insurance that may or may not actually cover anything

- Gas prices that feel like a subscription service you never signed up for

One example in the report highlights a $150,000 earner still paying hundreds out-of-pocket for a basic medical scan.

So no, this isn’t just a “low-income problem.”

It’s a cost-of-living problem that scales upward with you.

The Most Expensive Mistake: Trying to Keep Up

Let’s talk about the financial trap that keeps quietly catching people:

The “I’ll make it work” purchase.

Especially when it comes to cars.

- Average new car price: around $50,000

- Average payment: $700+

Most people look at that and say, “Absolutely not.”

So they compromise:

“I’ll just go cheaper.”

That’s how you end up with:

- Inflated used car prices

- Higher interest rates

- Unexpected repair bills

And suddenly, that “more affordable” option becomes a long-term liability.

The problem isn’t just the price.

It’s the pressure to maintain a lifestyle that no longer matches the math.

Owning vs. Renting: The Uncomfortable Truth

There’s another shift happening that would’ve sounded absurd a decade ago:

For many people, renting may now be the more financially rational choice.

Buying a home today often means:

- Higher monthly payments than rent

- Property taxes

- Maintenance costs

- Zero flexibility

Meanwhile, renting offers:

- Predictability

- Lower upfront costs

- The ability to invest elsewhere

For a growing number of Americans, the dream of ownership isn’t just delayed—it’s being reconsidered entirely.

Not emotionally. Financially.

So… Is This By Design?

That’s the question people are starting to ask.

Why does it feel like everyone is stuck in the same place?

Not failing.

Not thriving.

Just… maintaining.

The answer isn’t a grand conspiracy—it’s a system that rewards:

- Spending over saving

- Borrowing over owning

- Participation over independence

An economy built on consumption works best when people:

- keep working

- keep spending

- keep financing

Not when they get ahead and step off the treadmill.

The Bottom Line

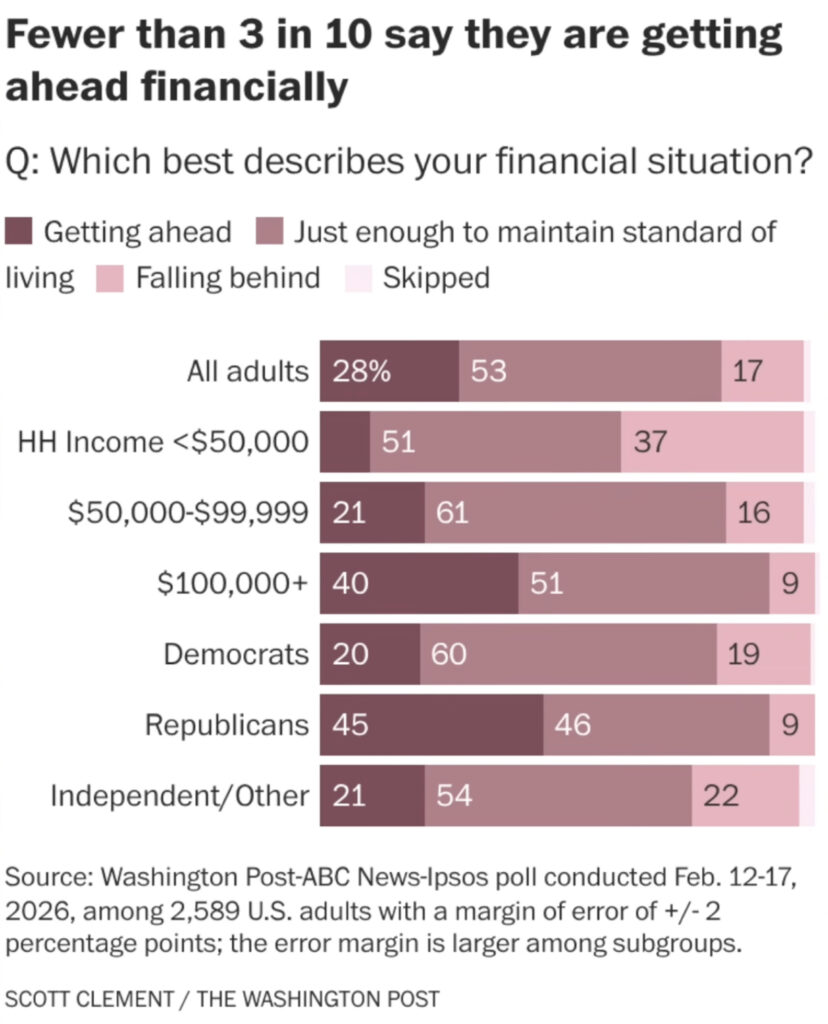

Right now, only about 28% of Americans say they’re getting ahead financially.

Everyone else?

They’re either:

- holding steady

- or slipping backward

That’s not collapse.

But it’s also not progress.

It’s something quieter—and arguably more frustrating:

A system where you can afford to live… but not quite afford a life.

If this continues, the biggest shift won’t just be economic.

It will be psychological.

Because once people stop expecting to get ahead…

They start playing the game very differently.

And that’s when things actually change.